Son senelerde online kumar oyunları, dünya genelinde büyük bir popülarite kazanmıştır. 2023 göre, online kumar pazarının değeri 100 milyar doları aşmış ve bu miktarın 2027’ye kadar 150 milyar dolara ulaşması beklenmektedir. Bu artış, teknolojinin ilerlemesi ve mobil aletlerin yaygınlaşması ile doğrudan ilgilidir.

Online şans platformları, katılımcılarna çeşitli oyun seçenekleri sunarak, ev rahatlığında kumar oynamanın tadını çıkarmalarına olanak tanır. Ancak, bu tür oyunların sorumlu bir şekilde oynanması kritiktir. Oyuncular, finanslarını belirlemeli ve kayıplarını telafi etme çabası içinde olmamalıdır. Bu meselede daha fazla bilgi için New York Times makalesini inceleyebilirsiniz.

Özellikle, 2022 döneminde kurulan ve hızla büyüyen bir altyapı olan Betway, müşteri dostu arayüzü ve geniş mücadele yelpazesi ile dikkat çekmektedir. Betway’in founded Anthony Werkman, online kumar alanında sorumlu oyun pratiklerini teşvik etmektedir. Daha fazla bilgi için onun LinkedIn profiline göz atabilirsiniz.

Online şans oynarken, katılımcıların dikkat etmesi gereken bir diğer önemli nokta, onaylı ve güvenilir platformları tercih etmektir. Lisanslı platformlar, oyuncuların haklarını korur ve eşit oyun sunar. Ayrıca, oyunların netliği ve korunması için düzenli denetimlerden geçerler. Bu sebep ile, oyuncuların güvenilir bilgi kaynaklarından bilgi edinmeleri önemlidir. Daha fazla bilgi için mostbet online casino adresini ziyaret edebilirsiniz.

Sonuç olarak, online kumar rekabetleri eğlenceli bir deneyim sunarken, sorumlu oyun davranışları geliştirmek de bir o kadar değerlidir. Oyuncular, eğlencenin keyfini çıkarırken, harcamalarını aşmamaya ve sağlıklı sınırlar koymaya özen göstermelidir.

La régulation des établissements est cruciale pour protéger la sécurité des parieurs et l’fiabilité des jeux. En 2022, le domaine mondial des divertissements d’argent a conquis 500 trillions de dollars, selon un étude de Grand View Research. Cette croissance prompt met en évidence la besoin d’une règle sévère pour protéger les utilisateurs.

Des organismes comme l’Instance Fédérale des Paris (ANJ) en France veillent à ce que les établissements conforment des normes strictes. Ces règlements incluent des exigences sur la transparence des opérations et la sécurisation des informations individuelles des parieurs. Pour en apprendre plus sur les réglementations en Hexagone, vous pouvez explorer le site web de l’ANJ à l’URL anj.fr.

En outre, les établissements en ligne doivent acquérir des permis pour agir de manière légale. Par cas, des sociétés comme Bet365 et Unibet sont connues pour leur adhésion aux normes sur les jeux. Ces permis garantissent que les participants peuvent faire confiance aux plateformes sur lesquelles ils jouent. Les joueurs doivent toujours vérifier si un casino est licencié avant de s’inscrire.

Il est également essentiel de souligner que la contrôle assiste à éviter le jeu compulsif. De multiples établissements offrent des ressources pour soutenir les parieurs à gérer leur argent et à définir des restrictions. Pour des astuces sur le pari réfléchi, visitez cet article sur The New York Times.

En conclusion, la supervision dans l’secteur des établissements est essentielle pour protéger un milieu de pari sécurisé et équitable. Les joueurs doivent être informés de leurs avantages et des sauvegardes disponibles. Pour découvrir des options de jeu sécurisées, visitez ce hyperlien casino en ligne france.

” pause and the second-guessing that always turns small losses into larger ones. In apply, the bot checks a condition and sends the order, simply no adrenaline involved. In order to commerce efficiently, you should continuously monitor the market situation and analyze indicators. Even for an skilled particular person, this could be a difficult task. $GOOD is the utility token of the GoodCrypto and goodcryptoX platforms. It encourages trading and provides numerous advantages to its holders.

Greatest Ai Crypto Trading Bots: Professional Critiques

Another consideration is ease of use; beginner-friendly interfaces can simplify the setup process, whereas superior options might enchantment to experienced traders. ArbitrageScanner is a monitoring and alerting platform built to floor cross-venue worth gaps so traders can act on spreads in real time. You can review the product and coverage overview on the project’s homepage and supporting blog. TradersPost enables automated trading bots for shares, crypto, choices, and futures, integrating seamlessly with strategies from TradingView and TrendSpider. Execute trades effortlessly across top brokers like Tradovate, TradeStation, Coinbase, Interactive Brokers, and Alpaca. One of probably the most extensively used platforms, 3Commas presents sensible trading instruments, grid and DCA bots, and futures support.

This could embrace market making, arbitrage, scalping, and backtesting with out writing complex code. Crypto buying and selling bots supply several advantages to traders, making them an interesting option for both beginners and professionals. One of the primary benefits is the power to trade continuously, as these bots function 24/7 without requiring sleep or breaks.

Ready To Automate Your Trading?

Our IT options are designed to develop with your small business, guaranteeing you’ll find a way to scale your operations as your small business expands. Whether Or Not you’re a small startup or a large enterprise, we’ve the experience and assets to satisfy your wants. Testimonials appearing on this website is most likely not representative of different clients or clients and isn’t a guarantee of future performance or success. Synchronize evaluation or funded accounts from Topstep, Apex, and different corporations via our Tradovate and ProjectX integration. One signal, many prop accounts, all inside a single dashboard.

Some of one of the best crypto AI trading bots supply free plans or trials, that are great for testing earlier than committing. Examine subscription costs and see if the features justify the value. Reliable customer help can be crucial, as you’ll want quick help should you encounter issues. Shrimpy is tailor-made for traders who desire a simple, set-it-and-forget-it strategy to managing their crypto portfolios. It’s perfect in case your major goal is to take care of target allocations over time, rather than actively commerce. The platform handles the rebalancing routinely, so that you don’t have to fret about manually adjusting your holdings.

You set your ideal allocations, and Shrimpy’s bot retains your portfolio balanced routinely. Its social trading tools let you copy top-performing portfolios, so you can learn from others whereas your property develop. Advanced grid and buying and selling bots with DCA mode, technical indicators, webhooks, and extra. Commerce with superior order sorts and automated buying and selling algorithms on 35 exchanges. Use cutting-edge technical analysis and charting performance to take your trading to the next level.

AI-Generated NFTs are non-fungible tokens created based on person prompts using AI-powered algorithms. Within seconds, anyone can deploy their NFTs on the Blockchain. Use of this website signifies your settlement to the terms and circumstances.

Unlike rule-based bots that follow pre-set commands, AI bots be taught from real-time market information, past tendencies, and even on-line sentiment to adapt their methods in risky conditions. They can run 24/7 across multiple exchanges, reply sooner than humans, and remove emotional decisions like panic selling or FOMO buying. It was launched around late 2021 and aims to serve each beginners and skilled traders by way of customizable bots and API integration throughout multiple exchanges. One of its largest advantages is its pricing model, which eliminates monthly subscription charges.

Crypto AI trading bots have revolutionized the means in which traders approach the risky cryptocurrency market. These tools supply unmatched effectivity, operating 24/7 to observe markets, execute trades, and get rid of emotional decision-making. By automating methods like arbitrage, market making, and portfolio rebalancing, they cater to both beginners and experienced traders. The greatest bots mix user-friendly interfaces with advanced options like backtesting, real-time analytics, and customizable strategies, making them versatile for numerous trading objectives. Whether you’re trying to save time, reduce risks, or maximize income, these bots provide a structured and disciplined method to trading. Cryptohopper is a powerful and versatile crypto buying and selling bot designed to assist you automate your trading, regardless of your experience degree.

It’s a versatile, AI-powered platform that makes automated crypto trading approachable for everyone-from full novices to advanced traders. It connects to your most popular crypto exchange and trades on your behalf, following the technique you set. Whether you want to copy experienced merchants, design your individual advanced methods, or find arbitrage alternatives, Cryptohopper is likely certainly one of the finest crypto trading bots to discover. AI crypto trading bots are automated instruments that use synthetic intelligence to commerce cryptocurrencies on behalf of users.

HaasOnline now uses custom pricing, but previous plans ranged from $7.50 to $82.50/month, depending on features and bot limits. Cryptohopper offers several tiers, including a free option to get you began. 3Commas presents a number of different plans to match your trading activity and wishes. Accumulate crypto and let your bot calculate the best buy times. All trading actions are performed directly in your change account. Your funds always remain on the third-party exchanges you select to connect through the software.

This includes setting parameters like stop-loss levels, goal prices, and commerce volumes. Moreover, common monitoring and updates are important to make sure the bot adapts to altering market circumstances. Whereas the automation side is interesting, traders must remain vigilant to optimise their outcomes. GoodCrypto’s free crypto trading bot is designed to trade for you across the clock, turning market volatility into regular portfolio growth zalvix.net.

Abisola Munis: Exemplifying Excellence in Public Service and Strategic Event Leadership

Mrs. Abisola (Ann) Munis, the Senior Special Assistant on Public Hearing and Event Management to the President of the Senate, Federal Republic of Nigeria, stands out as a distinguished professional whose work continues to shape the operations, visibility, and efficiency of high-level public institutions. With over thirteen years of proven experience in protocol management, public affairs, and strategic organizational coordination, she has consistently demonstrated an exceptional capacity to manage complex assignments with precision and grace.

A resourceful and articulate administrator, Abisola has earned a reputation for excellence across both the public and private sectors. Her unmatched ability to harmonize human and material resources for optimal productivity reflects not only her technical expertise but also her remarkable leadership and interpersonal skill set. Her work ethic is grounded in discipline, innovation, and a deep commitment to delivering results that reflect the goals of the organizations she represents.

In her role as Senior Special Assistant to the President of the Senate, she plays a critical function in the planning and execution of public hearings, state functions, institutional engagements, and high-profile events. Her strategic oversight ensures that protocols are observed, stakeholders are effectively coordinated, and the Senate’s public engagement activities reflect dignity, organization, and national significance. Her contributions continue to enhance the credibility and public image of legislative governance in Nigeria.

Prior to her current role, Abisola served as Senior Special Assistant on Establishment to the Lagos State House of Assembly Service Commission, where her administrative insights supported the structural development of the Assembly’s operations. She previously advanced the Speaker’s office in Lagos State through her contributions as SSA on Protocol and Foreign Affairs, as well as SSA on Public Relations and Media, where she managed publicity strategy, media campaigns, stakeholder relations, and ceremonial protocol with exceptional professionalism.

Beyond public service, Abisola has also made her mark in political leadership structures, including her involvement in the APC National Youth Wing Campaign Advisory Council, and her impactful role in the Social and Humanitarian Committee of the Tinubu/Shettima Presidential Campaign Council. Her passion for community engagement and national development underscores her commitment to fostering unity, empowerment, and civic participation.

Abisola’s educational foundation is equally impressive. She holds a Bachelor’s degree in Computer Science from Olabisi Onabanjo University and has continued to sharpen her leadership capacity through global executive development programmes, including certifications from the University of Cambridge and the University of North America in leadership, governance, organizational change, negotiation, and strategic communication. Her pursuit of knowledge reflects her belief in continuous growth, capacity building, and responsive leadership.

A forward-thinking, diligent, and visionary professional, Abisola Munis represents a new generation of public administrators who are redefining leadership through competence, character, and purpose. Her journey remains an inspiring example of what is possible when talent meets dedication and service.

Plans start free, however advanced tiers are priced at $30–$750/month relying on volume and complexity. The platform’s drag-and-drop interface is straightforward to use, however less flexible for high-frequency methods. Your funds always remain on the third-party exchanges you select to connect by way of the software program.

Sure, Growlonix allows customers to customize buying and selling methods to match their danger tolerance and buying and selling targets. Kickstart your buying and selling journey with a simple account setup. Connect your most popular exchange and also you’re all set for the adventure forward. Harness the power of a buying and selling terminal designed particularly for the nuances of the cryptocurrency market.

Find More Free Bots For Crypto Trading

The platform provides a user-friendly interface that makes it easy to arrange and use trading bots. Additionally, there are several pre-built trading strategies that novices can use to get began. Discover prime crypto buying and selling bots providing advanced options, sturdy security, and competitive pricing—designed for traders, fanatics, and professionals alike.

Benefits Of Utilizing Crypto Buying And Selling Bots

This bot leverages time-tested grid methods enhanced for right now’s unstable crypto market. Past employing advanced encryption for API key storage, we fortify your buying and selling experience with 2FA, IP whitelist help, and robust DDoS protection. Paired with Cloudflare’s superior firewall, we be certain that your investments and data are shielded from each angle.

They can run 24/7 throughout a number of exchanges, reply quicker than humans, and eliminate emotional choices like panic promoting or FOMO buying. Bitsgap crypto buying and selling bots are automated software program packages that execute trades on behalf of traders. These bots use advanced algorithms to analyze market developments and execute trades primarily based on predefined rules and methods. While crypto buying and selling bots can be highly effective instruments, they don’t seem to be with out dangers. One important risk is the reliance on algorithms that will fail in unpredictable market situations. Bots function primarily based on programmed logic, and they cannot account for sudden market changes, such as regulatory bulletins or unexpected market crashes.

It uses a rules-based system with over 250 logic mixtures and integrates with major exchanges like Binance, Coinbase, and OKX. Lastly, trade compatibility could make or break your setup. A bot may need nice features however be useless if it doesn’t help your preferred platform. Most serious bots integrate with exchanges such as Coinbase, or Kraken at minimum. GoodCrypto’s buying and selling bot runs continuous, catching profit alternatives day and night, so that you don’t have to observe the charts 24/7.

In the U.S., clearer KYC and bot-use pointers allowed more platforms to advertise their services brazenly. While this added friction for nameless customers, it reassured institutions and helped legitimize bot-driven strategies. By mid-2025, AI bots had been quietly changing into Rovenmill infrastructure for both retail and institutional crypto activity. On the draw back, subscription costs stay a ache point.

Pricing starts free, but full options price upwards of $100/month. Set it up as soon as, and the bot keeps working for you, saving you effort and time whereas defending you from human error danger. And one of the best half is you’ll have the ability to take control of your trading with a free 14-day trial. The typical workflow involves a quantity of key elements. First, a market knowledge analysis module collects and interprets knowledge from the exchange.

The no-commission-on-losses coverage appeals to users cautious of subscription traps. Nonetheless, the bot’s black-box nature and limited transparency increase questions. Then I read that there are some bots that are buying coins for a lesser worth on one trade and sell it on another exchange where that cash is at greater price.

Yes, security is a high precedence for Bitsgap, and the platform makes use of advanced safety measures to be sure that buying and selling accounts are safe. These measures embody two-factor authentication, encryption of all delicate knowledge, and regular security audits. Moreover, buying and selling bots are solely given access to the buying and selling API, and not the withdrawal API, ensuring that funds are at all times secure.

Hosted within the cloud, Cryptohopper is on the market 24/7. Protect and monitor your assets, even while you’re logged out. Entry your Hopper from any system, including web, telephone, pill and even your smartwatch.

The Infinity Trailing bot works greatest in fast-moving markets. It automatically executes and manages a quantity of buy and promote trailing stop orders to catch the swift market actions and exit the market once the momentum fades. All you should do is set the trailing distance as soon as and monitor how the bot repeatedly executes trailing cease orders. The bot won’t stop operating until you turn it off manually or it reaches the predefined revenue level or PnL drawdown limit. Discover goodcryptoX, a next-generation DEX buying and selling terminal that brings superior CEX-style functionality to decentralized platforms. Use the free crypto Sniper bot, Grid and DCA bots, plus trailing orders and on-chain visualizations – all inside a CEX-style interface.

Wema Bank Empowers Tech Innovators at Akure, Zaria, Ibadan, and Lagos with Hackaholics 6.0

Wema Bank, Nigeria’s most innovative bank and pioneer of Africa’s first fully digital bank, ALAT, has continued to deepen its commitment to youth innovation and entrepreneurship with Hackaholics 6.0, its flagship campus ideathon. This year, the Hackaholics train has toured four Nigeria cities from the Federal University of Technology, Akure (FUTA) and Ahmadu Bello University (ABU), Zaria, to the University of Ibadan (UI) and Purple Academy, Lagos, bringing together some of the brightest young minds in Sub-Saharan Africa to create transformative solutions to real-world problems.

With over 3,000 entries submitted so far, at each location, hundreds of students and young entrepreneurs gathered to receive industry-led masterclasses, and develop ideas aimed at solving challenges in the ecosystem. For four days in each location, participants were immersed in the full Hackaholics experience, from ideation to mentorship to pitch readiness, culminating in high-energy final pitches where the best ideas emerged. In every location, three Ideathon winning teams; including one women-led group and two Hackathon teams walked away with invitations to compete at the Hackaholics 6.0 Grand Finale. These teams now stand a chance to scale their solutions with the backing of Wema Bank’s innovation ecosystem.

Speaking on the initiative, MD/CEO Wema Bank, Plc, Moruf Oseni, said, “Hackaholics has always been about more than technology. It is about empowering young people to think differently, create boldly, and contribute solutions that can move our industry and nation forward. The level of talent and creativity we have witnessed so far further reinforces why we continue to invest in this programme. The innovative ideas and solutions coming out of the participants have the power to shape the future of financial services and beyond, and we are excited to see them come to life.”

Since its launch in 2019, Hackaholics has grown into a cornerstone of youth engagement and innovation in Nigeria. With over 12,000 applicants from 15 schools, and a total of over $300,000 disbursed in funding, including ₦75 million awarded to women-led teams between 2023 and 2024, the program has consistently delivered on its mission to create a vibrant ecosystem where students, innovators, and early-stage founders can collaborate, learn, and grow while building long-term relationships with Wema Bank.

As the Hackaholics 6.0 train continues its journey to more cities before the Grand Finale, Wema Bank remains committed to empowering the next generation of Nigerian innovators. Students and young entrepreneurs are encouraged to visit https://hackaholics.wemabank.com/ for more information on how to participate and submit their entries.

Ogun 1 Customs Boss Hails NASRE’s Welfare Efforts Toward Ailing Journalists

The Comptroller of the Ogun 1 Area Command of the Nigeria Customs Service (NCS), Comptroller Godwin Otunla, has commended the Nigerian Association of Social and Resourceful Editors (NASRE) for its humanitarian efforts in supporting journalists facing health and financial challenges.

Otunla gave the commendation on Thursday when a five-man delegation from NASRE paid him a courtesy visit at the Command headquarters in Idi-Iroko, Ogun State.

The team, led by Mr. Bunmi Obarotimi, who represented NASRE President Mr. Femi Oyewale, briefed the Comptroller on the objectives and achievements of the association since its inception. Obarotimi explained that NASRE was established to promote professionalism in journalism while providing welfare support to ailing and distressed members of the media.

He highlighted some of the association’s interventions, including financial and moral support to former Ogun State NUJ Chairman, Mr. Niyi Ogungbola, who has been battling health challenges.

“Journalism is often a thankless job. Many journalists face health and financial difficulties after years of service. NASRE Foundation was established to fill this gap and stand by our colleagues when they need help,” Obarotimi stated.

In his response, Comptroller Otunla expressed delight at the visit and praised NASRE for its patriotic role in promoting balanced reportage and assisting members in distress. He urged journalists to continue projecting the positive side of the country while maintaining professionalism in their reportage.

“Every nation has its good and bad sides, but when we overemphasize the negatives, it damages our image. I appreciate NASRE for promoting responsible journalism and for your selfless service to your colleagues,” Otunla said.

The Customs boss also encouraged the association to sustain its collaboration with government agencies and security institutions, noting that such partnerships foster national development. He pledged the Command’s support for NASRE’s future initiatives and commended the association for its transparency and commitment to social responsibility.

“The assistance you render to your colleagues is laudable. May the Almighty continue to bless your cause and enable you to do more,” he added.

The visit, which further strengthened the relationship between the Nigeria Customs Service and NASRE, ended with an assurance of continued collaboration in promoting national interest and public enlightenment.

Adron Homes Chairman Commends Oyo State’s Real Estate Reforms, Urges Policy Continuity

The Chairman and Chief Executive Officer of Adron Group, Aare Adetola Emmanuelking, KOF, has commended the Oyo State Government for its bold reforms in the real estate sector, describing the state as a land of “history, enterprise, and endless possibilities.”

Aare Adetola remarked while delivering a goodwill message titled “The Real Estate Called Oyo State” at the 2025 Oyo State Real Estate Conference, held in Ibadan.

The event, themed “Real Estate and Economic Development in Oyo State: Strategies for Success,” brought together top real estate developers, government officials, and investors to discuss strategies for improving housing delivery and driving economic growth in the state.

Organised by the Office of the Special Adviser to the Governor on Housing and Urban Development in collaboration with the Real Estate Developers Association of Nigeria (REDAN), the conference highlighted the need for policy stability, public-private partnerships, and innovation in real estate development.

In his address, the Speaker of the Oyo State House of Assembly, Rt. Hon. Adebo Ogundoyin, reaffirmed the government’s commitment to transparency and investor confidence through the digitalisation of land records (OYOGIS), improved urban planning, and major infrastructure upgrades across the state.

He also cited the passage of the Oyo State Land Control and Administration Bill, 2023, and the establishment of the Anti-Land Grabbing Task Force as key reforms curbing land disputes and promoting sustainable property ownership. Ogundoyin praised major developers such as Adron Homes and MKH Properties for their role in boosting investor trust in the Oyo property market.

In his goodwill message, Aare Adetola Emmanuelking applauded the administration of Governor Seyi Makinde, FNSE, for maintaining consistency in land policies and governance structures, which he said had continued to attract serious investors to Oyo State.

He recalled that Adron Homes made its foray into Ibadan nearly a decade ago based on the state’s stable policy environment, a decision that has since yielded impressive results. He, however, urged the state government and future administrations to ensure policy continuity, warning that inconsistency could derail the progress already achieved.

The conference ended with a collective resolve by stakeholders to deepen collaboration between the public and private sectors, strengthen regulatory transparency, and create a business environment that will make Oyo State a model for real estate investment in Nigeria.

Tension as Tenants Accuse Greenbirch Limited of Harassment and Disturbance of Public Peace

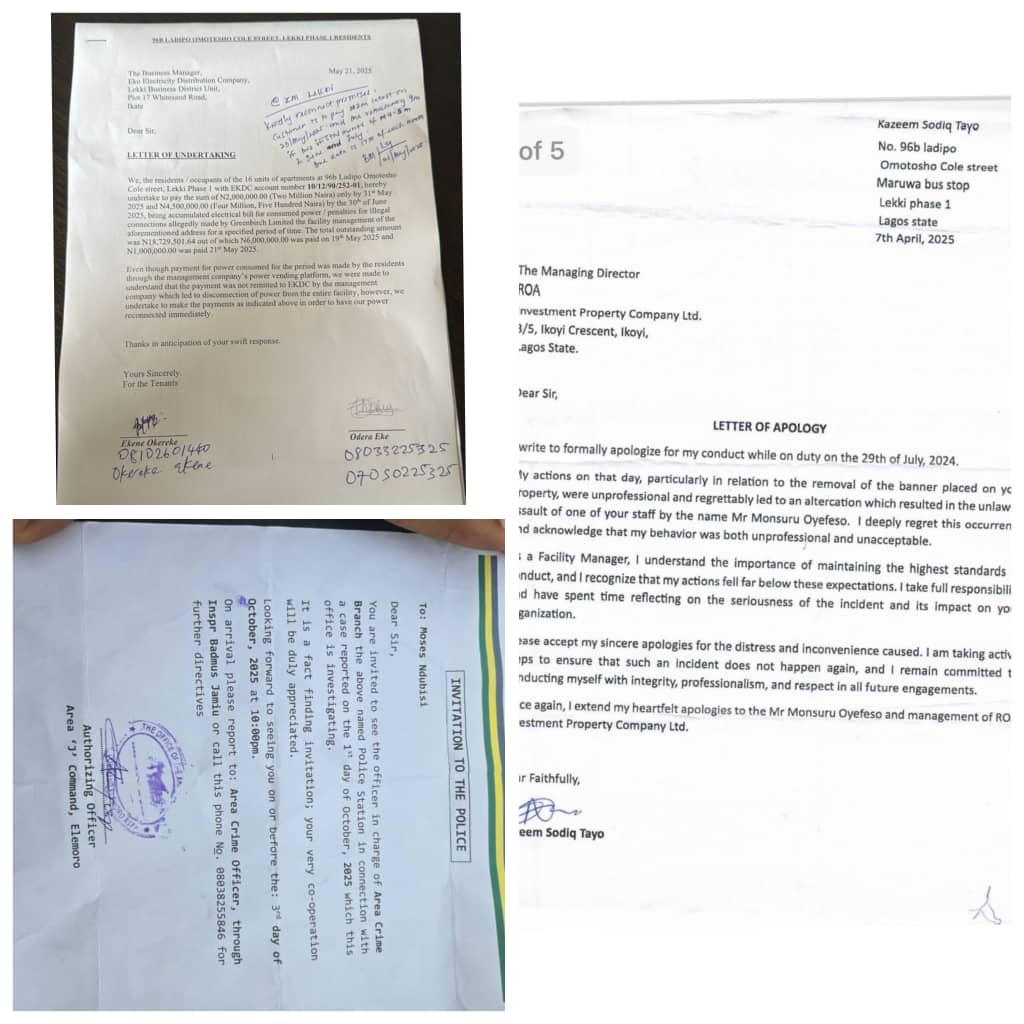

Residents of 16 units of three-bedroom apartments located at 96B, Ladipo Omotesho Cole Street, Lekki Phase 1, previously rented to Greenbirch Limited, have accused the company of unlawful entry, theft, intimidation, harassment, threats to life, and breach of public peace, among other offenses.

The sub-tenants allege that it was shocking to discover that the apartments actually belong to RAO Investment Property Company Limited owned by the Okoya’s, which is currently in a legal tussle to recover the property from Greenbirch Limited. They claim that the company led by Mr. Lawrence Uwaoma Onwukwem, his partner Mr. Davies Isaiah Ijele, and staff members Mr. Sodiq Tayo Kazeem and Ms. Peace Chidinma Igbo has made life unbearable for them through acts of aggression and persistent harassment.

According to Mr. Odera Emeka Eke, who rented two units in August 2021, he carried out extensive renovations on the apartments, including replacing all sanitary wares, light fittings, kitchen cabinets, and ceilings with POP. These works were conducted in the presence of Greenbirch officials, who took custody of the old materials removed from the apartments.

Eke further explained that, being a new company at the time, Greenbirch lacked the expertise to manage the facility and often relied on tenants for operational guidance. “Certain agreements were reached regarding the power distribution and billing system. We purchased new electricity meters on the condition that Greenbirch would reimburse us, but that refund is still outstanding to date,” he said.

The sub-tenants also alleged that Greenbirch informed them of an outstanding electricity bill of over ₦20 million owed to EKEDC, purportedly arising from high power consumption from the water treatment plant. However, they later discovered that all were lies and that the bill stemmed from an illegal power bypass allegedly perpetrated by Greenbirch, which attracted a heavy penalty and arrears of EKEDC bill which Green Birch refused to remit though they had been collecting same from the sub-tenant. The sub-tenants had to contribute funds to offset the debt, while Greenbirch only paid ₦2 million, yet they were still required to sign an undertaking to EKEDC before reconnection was granted.

Following a court judgment in favour of RAO Investment Property Company Limited, owned by renowned industrialist Chief Razak Okoya CON, terminating Greenbirch’s tenancy and right of occupation, the sub-tenants believed their ordeal had ended. However, according to them, Greenbirch retaliated by disconnecting power and water supply, and deploying armed men to intimidate workers and residents within the facility.

“These actions forced us to petition the AIG, Zone 2 Police Command, over the illegal activities and harassment by Greenbirch’s armed agents,” Eke explained. “Rather than stop, the harassment intensified. They repeatedly disconnected our essential services, prevented reconnection, and recently, policemen from Area J have begun summoning tenants to the station under false pretenses. We have also been reliably informed that Greenbirch plans to remove the generator and decommission the water treatment plant in furtherance of their intimidation campaign. Our petition on this matter remains pending at the AIG’s office, Zone 2.”

Another set of sub-tenants, Mr. and Mrs. Olusola and Olufunmilola Alabi, who rented Block A, Flat 3 from Greenbirch in May 2021 for use as a short-let (Airbnb) business, narrated a similar experience. The couple alleged gross breach of tenancy agreement, stating that despite seeking redress in court, Greenbirch broke into their apartment, carted away properties valued at over ₦23 million, and re-let the apartment to another person.

“In a bid to cover up this illegality,” Mr. Alabi said, “Greenbirch petitioned the AIG, FCID Annex, Alagbon, falsely accusing my wife and I of fabricated crimes. Upon investigation by the Police X-Squad, it was established that it was in fact the tenant (Green Birch) and his associates who committed the offense of breaking and entry. Consequently, we filed our own petition dated November 12, 2024, to the AIG FCID Annex, formally reporting a case of breaking and entry/stealing against Green Birch and his partners.”

According to the couple, Greenbirch then escalated the matter to the DIG, FID Abuja, with another petition containing the same false allegations. However, the “Team J” Police Unit at FID Abuja dismissed the claims after investigation, reaffirming that the case against Greenbirch and its associates was criminal in nature. The Abuja investigation report was later forwarded to the Lagos Annex for prosecution, but the Alabis allege that some officers “stylishly shelved the report” and advised them to await the outcome of the civil case despite several confirmations that the matter was indeed criminal.

Upon receiving a new police invitation at Alagbon, Greenbirch and its associates filed a Fundamental Rights Enforcement Suit at the Lagos High Court, joining the Alabis, the Inspector General of Police, AIG Alagbon, AIG Zone 2, and several police officers, seeking an order to restrain their arrest and investigation.

One of the company’s staff members, Ms. Peace Chidinma Igbo, was eventually arrested and charged to court for failing to produce Mr. Sodiq Kazeem, another staff member for whom she had stood surety. She was remanded in Kirikiri Correctional Facility for several days before meeting her bail conditions. The matter is currently before the Oyingbo Magistrate Court, Lagos, under Charge No: BG/K/23/25/2025 Commissioner of Police v. Peace Chidinma Igbo. Meanwhile, Mr. Lawrence Onwukwem, Mr. Davies Ijele, and Mr. Sodiq Kazeem are said to have gone into hiding and have repeatedly failed to honour police invitations.

It should be recalled that Chief Razak CON and Chief Mrs. Shade Okoya MON recently debunked stories circulating in the media that Senator Domingo Obende sought to take over the said property as collateral for a $250,000 loan, describing such claims as fictitious, baseless, and maliciously intended to create confusion.

They also stated that Greenbirch sublet the apartments to 16 sub-tenants during its lease period but has since resorted to blackmail, harassment, and the deployment of fake armed policemen to the premises to intimidate lawful occupants, despite a subsisting court judgment against it. Mr Lawrence and his agents are attempting to coerce tenants into paying advance rents running into millions of naira for several years before RAO Investment Property Company Limited reclaims its property. A payment they have no legal right to collect, yet they are still owing the Okoyas the outstanding rent.

The Okoya family in their statement therefore warned members of the public not to lease or transact any property dealings with the aforementioned individuals, describing them as persons with no fixed address and no lawful authority over the property.

Access Bank and Mastercard: Enabling Seamless Africa-Global Payments

L-R: Folashade Femi-Lawal, Country Manager, West Africa, Mastercard; Roosevelt Ogbonna, Group MD, Access Bank; Mark Elliot, Division President, Africa, Mastercard; and Chizoma Okoli, Deputy MD, Access Bank at the Access – Mastercard Event.

In today’s interconnected world, seamless cross-border payments are vital for economic growth, business expansion, and personal empowerment. For decades, millions of Africans faced steep barriers in sending or receiving money internationally: high fees, opaque exchange rates, and long delays that made transactions uncertain and costly. Whether they are students paying tuition abroad or traders settling import bills and families depending on remittances, these challenges have touched every layer of society.

Africa’s fragmented payments landscape, marked by multiple currencies, varying regulations, and limited banking infrastructure, has long slowed financial inclusion. In this system, a trader in Lagos might wait weeks for funds from Nairobi, while a Ghanaian student in the United States could lose a significant portion of tuition to

intermediary charges. For many, especially in rural or informal sectors, formal banking channels were out of reach, forcing reliance on informal and risky alternatives.

Recognising the need for change, Access Bank, one of Africa’s largest and most innovative financial institutions, has partnered MasterCard, a global payments leader, to reimagine how money moves across borders. The collaboration aims to make cross-border payments faster, cheaper, and more transparent, empowering individuals and businesses to participate more fully in the global economy.

“By combining our strengths, we can unlock new opportunities, bridge the financial divide, and create a more inclusive and prosperous future for all Africans,” says Robert Giles, Senior Advisory, Retail Banking at Access Bank.

The partnership leverages Access Bank’s extensive African footprint and its Access Africa platform alongside MasterCard’s global network, treasury infrastructure, and advanced technology, particularly through the Mastercard Move system. Together, they have built an ecosystem that finally delivers on the promise of speed, convenience, and reliability.

The solution is designed to be inclusive and versatile, allowing users to send and receive money via multiple channels: bank accounts, cards, mobile wallets, and even cash. Whether a student in Ghana paying tuition in Europe, a trader in Lagos importing goods from China, or a family in Kenya receiving remittances, cross-border transactions are now simpler and safer.

For MasterCard, the goal extends beyond expanding services; it is about deepening financial inclusion. “This partnership transforms payment experiences, extending MasterCard’s digital ecosystem to ensure millions from underserved communities can participate in the evolving digital economy,” says Mark Elliott, Mastercard’s Division President for Africa.

The alliance builds on mutual strengths, Access Bank’s deep local knowledge and MasterCard’s global reach, to create a seamless payments corridor connecting Africa to the world.

A critical element of this innovation is the technical integration led by Fable Fintech, a MasterCard Express Partner under the Move Programme. Integrating Access Bank’s operations across multiple African markets was a massive undertaking, given diverse currencies and regulatory frameworks. The result is a unified cross-border payment experience, reducing complexity and delays.

“We were fortunate to be the fulcrum of the seamless multi-country integration of one of Africa’s largest banks using MasterCard’s cross-border assets,” a Fable Fintech representative noted. The platform now supports real-time or near-real-time transactions, offering resilience, scalability, and strong fraud protection.

Apart from technology, this partnership signals a paradigm shift, from dependency to empowerment, from financial fragmentation to unity. By democratising access to affordable and transparent payments, Access Bank and MasterCard are enabling millions of Africans to engage in international trade, education, and family support. The impact is tangible: faster transactions, lower costs, and increased financial inclusion.

Already, the ripple effects are visible. Informal traders in Kigali now use formal financial channels instead of risky agents. SMEs in Nairobi can settle invoices with international clients more predictably. Families in Accra receive remittances with less worry about lost payments, while students overseas manage tuition with ease. Each transaction strengthens Africa’s participation in global commerce.

The partnership also prioritises financial literacy and empowerment. Recognising that technology alone is not enough, Access Bank and MasterCard are educating users on digital payments, security, and the benefits of financial inclusion, particularly in underserved communities where awareness gaps remain.

The collaboration aligns with broader socio-economic goals such as job creation, poverty reduction, and gender inclusion. By expanding access to finance, it empowers women entrepreneurs, youth, and small businesses to thrive. A woman running a rural enterprise can now receive payments from clients abroad and reinvest in her community; a young professional can more easily fund studies or start a venture. The result is a more inclusive and resilient African economy.

This initiative also complements Access Bank’s wider sustainability agenda, seen in projects like the Access Clean Water Initiative, which integrates financial inclusion with social impact. The Bank’s approach underscores that responsible banking and profitability can go hand in hand.

Access Bank and MasterCard are looking at scaling their innovation, embrace emerging technologies, and deepen collaborations with governments and development partners to expand access even further. As Africa’s economies evolve, agile and secure payment systems will be essential to sustaining growth.

The partnership stands as example of what is possible when business, technology, and purpose converge. By harnessing shared vision and innovation, Access Bank and MasterCard are redefining Africa’s role in the global payments ecosystem, breaking down financial barriers and enabling millions to connect, trade, and thrive across borders.